A good budget can help when the unexpected occurs. But when you suddenly lose income, as many families have in recent months, a budget becomes even more important.

"Budgets change all the time," says Molly Barackman-Eder, senior manager in financial capability at NeighborWorks America. "If you've had a change in income, this is a good time to think about a budget as an organizing tool."

NeighborWorks network organizations say they are continuing to hear from residents interested in doing the financial education and credit repair that will help them on a path to buying new homes. But even before March turned to April, housing counselors say they were also receiving calls from residents who were worried about what was going to happen if. If they lost jobs. If they couldn't pay their rent or their mortgage as the COVID-19 virus forced businesses to shut down or scale back.

Some tax preparers call it "the big money moment." They're talking about the time of year when consumers receive their tax refunds. The lump sum, especially if the individual qualifies for the Earned Income Tax Credit (EITC), is often the largest payment they'll get all year long, says Molly Barackman-Eder, senior manager for financial capability at NeighborWorks America.

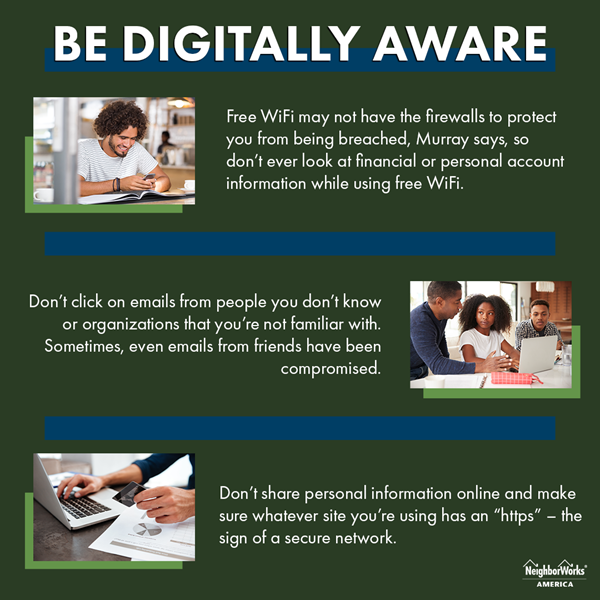

National Consumer Protection Week is a time for people to focus on finances and make sure they're making the right decisions to keep those finances healthy. But the things that lead us to make bad decisions or fall victim to credit problems or scams can happen all year round.

National Consumer Protection Week is a time for people to focus on finances and make sure they're making the right decisions to keep those finances healthy. But the things that lead us to make bad decisions or fall victim to credit problems or scams can happen all year round.

Payday and auto title loans offer a quick way to get money, but they come at a high cost. To make matters worse, they often must be repaid in a matter of weeks. Across the country, 12 million adults use payday loans annually, according to a study by Pew Charitable Trusts.

Having poor credit or no credit history at all can have ripple effects for a person who is already in a precarious financial situation. A person's credit history tells a story to lenders, landlords, and service providers; therefore, a poor credit history can make it difficult to find affordable housing, buy a home, or even procure common goods and services such as a cellphone, furniture, or car insurance.

p.p1 {margin: 0.0px 0.0px 0.0px 0.0px; font: 16.0px Times} p.p2 {margin: 0.0px 0.0px 0.0px 0.0px; font: 16.0px Times; min-height: 19.0px} span.s1 {font-kerning: none}

Molly Barackman-Eder, Manager, Financial Capability

The winter holidays and the start of school are times when expenses can suddenly spike. Many low- to moderate-income families are unable to cover them, turning instead to expensive, predatory payday, auto-title or similar loans. Clearly, a safe alternative is needed.

Get the latest in housing and community development trends and news.

Visit the NeighborWorks' store for homeownership resources.

Connect With Us

![]()

1255 Union St. NE, Suite 500

Washington, DC 20002

202-760-4000